So, you're holding stablecoins like USDC. That's great for stability, but let's be honest—if your digital dollars are just sitting in a wallet, they're not really working for you. They're just "parked," not growing.

This is where the world of Decentralized Finance (DeFi) comes in. It offers a powerful way to turn those static stablecoins into an active source of passive income. Think of it like a high-yield savings account, but built on the blockchain, accessible globally, and often with significantly higher returns than what you'd get from a traditional bank.

How to Start Earning DeFi Stablecoin Interest

The concept is actually pretty simple. In the old world, a bank takes your deposits, lends them out for a higher rate, and gives you a tiny slice of the profits. DeFi protocols essentially cut out that middleman.

When you deposit your stablecoins into a DeFi protocol, you're directly providing capital to lending markets or trading pools. In return for your liquidity, you earn a much larger share of the interest and fees that the protocol generates.

A Modern Alternative to Savings

For a growing number of people, earning interest on stablecoins in DeFi has become a serious replacement for their old-school high-yield savings accounts. The appeal comes down to a few key differences that really favor the DeFi approach, especially if you're comfortable with digital assets.

Some of the biggest advantages include:

Higher Potential Yields: DeFi protocols can offer interest rates that blow traditional savings accounts out of the water. This reflects the real-time supply and demand within the on-chain economy.

Global Accessibility: Forget geographical borders or banking hours. Anyone with a crypto wallet and an internet connection can tap into these opportunities 24/7.

Radical Transparency: Every transaction and the inner workings of the protocol are recorded on a public blockchain. You can literally verify everything yourself—from where the yield is coming from to the total funds in a pool.

You're in Control: It's your money, and you have self-custody. There are no tellers, no withdrawal limits, and no third party you need to ask for permission to move your funds.

The core idea is simple but powerful: instead of letting your money sit idle in a bank account earning minimal interest, you can put it to work 24/7 in a transparent, global financial system.

Of course, these benefits come with a different flavor of risk compared to a government-insured bank account. Getting a handle on this trade-off is the first and most important step before you dive in.

To make it crystal clear, let's stack them up side-by-side.

DeFi Stablecoin Yielding vs Traditional Savings

Feature | DeFi Stablecoin Interest | Traditional Savings Account |

|---|---|---|

Typical APY | Variable, often 3% - 15%+ | Typically 0.5% - 5.5% |

Accessibility | Global, 24/7 access | Region-locked, banking hours |

Transparency | Fully on-chain, auditable | Opaque, internal bank operations |

Custody | Self-custody (you hold keys) | Bank-custodied (third-party) |

Underlying Risk | Smart contract & protocol risk | Inflation & institutional risk |

Insurance | None (protocol-specific covers exist) | FDIC/government insured (up to a limit) |

As you can see, the trade-off is clear: DeFi offers higher potential returns and greater control in exchange for taking on smart contract and protocol-level risks that don't exist in traditional finance.

So, where does the interest on your stablecoins actually come from? Unlike a traditional bank where everything happens behind closed doors, DeFi is wide open. Your DeFi stablecoin interest isn't magic money; it's generated by real economic activity you can see on the blockchain.

It mostly comes down to two powerful engines: lending demand and trading fees. These two activities are what turn your passive stablecoins into active capital that powers the entire decentralized economy. Let's break down how each one works.

The Lending Engine: An Automated Global Pawn Shop

The most common way to earn yield is through lending and borrowing protocols like Aave and Compound. The best way to think of these platforms is as fully automated, global pawn shops that never close their doors.

You, as the lender, supply your stablecoins (like USDC or USDT) to the protocol's big pool of capital. Other users who want to borrow—but don't want to sell their crypto assets like Bitcoin or Ethereum—come to this "pawn shop." They lock up their crypto as collateral and borrow your stablecoins against it.

Key Concept: Over-collateralization Borrowers have to deposit collateral that’s worth way more than the amount they're borrowing. For example, to borrow $10,000 in USDC, a user might have to lock up $15,000 worth of ETH. This big buffer is what protects your capital if the market gets volatile.

These borrowers pay interest on the money they take out. Since you supplied capital to the pool, you get a cut of that interest, which is paid to you as yield. It’s a direct, peer-to-peer system where your money meets market demand, and you earn from it. This is the bedrock of how sustainable DeFi stablecoin interest is generated.

And the scale of this is immense. Stablecoins have become the essential oil for the DeFi machine, hitting a massive $320 billion market cap with staggering transaction volumes. A huge chunk of this, 56%, flows directly through DeFi protocols, where stablecoins are used for everything from simple borrowing to complex trading strategies.

The Trading Fee Engine: Powering Marketplaces

The second major source of yield comes from providing liquidity to decentralized exchanges (DEXs), like Uniswap or Aerodrome. Picture a busy foreign exchange kiosk at an international airport. It needs a constant supply of different currencies on hand to let people make trades.

A DEX is just like that, but for digital assets. To allow users to seamlessly swap one token for another (say, USDC for ETH), the DEX needs a ready pool of both assets. This is where you, as a liquidity provider (LP), step in.

You Provide the Inventory: You deposit your stablecoins into a liquidity pool, usually paired with another asset like ETH or even another stablecoin (like in a USDC-USDT pool).

Traders Use Your Inventory: When someone wants to make a trade, they tap into your pool, swapping one of your assets for the other.

You Earn the Fees: For every single trade, the DEX charges a small fee, typically around 0.05% to 0.30%. As a liquidity provider, you earn a share of those fees based on how much you contributed to the pool.

By providing liquidity, your stablecoins become the essential stock that makes thousands of daily trades possible. The interest you earn is your reward for making the market work. You can read more about typical stablecoin interest rates and see how much they can vary between different strategies.

At the end of the day, whether it's through lending or providing liquidity, your DeFi stablecoin interest is a direct payment for the valuable service your capital provides to a thriving on-chain financial world. No magic, just pure economics.

Navigating The Current DeFi Yield Landscape

If you've spent any time in DeFi, you know that stablecoin interest isn't a fixed number. It’s a living thing, always shifting with the mood of the wider crypto market. Those eye-popping yields you hear about aren't guaranteed; they’re a direct result of market sentiment, how much risk people are willing to take, and the classic push-and-pull between capital supply and borrowing demand.

Think of it like tides—yields rise and fall. When the market is bullish and everyone’s a trading genius, people are scrambling to borrow stablecoins to leverage up their bets. This massive demand, combined with a limited supply of lendable cash, sends interest rates through the roof. It’s these moments that often pull new investors into the space.

But when the mood sours and uncertainty creeps in, the whole thing flips. This is what we call a "risk-off" market.

The Impact Of A Risk-Off Market

In a risk-off phase, traders and institutions get cautious. Instead of borrowing to chase risky trades, they park their funds in stable assets for safety. Suddenly, lending protocols are flooded with stablecoins, with way more people looking to lend than to borrow.

When supply massively outstrips demand, the interest rates paid to lenders naturally have to come down.

We’ve seen this play out in recent market cycles. DeFi stablecoin interest rates have dropped significantly from their previous highs, acting as a clear indicator of how expensive it is to get leverage in crypto. It signals a ton of liquidity sitting on the sidelines with very little demand from borrowers, wiping out the temporary yield spikes we saw during smaller booms.

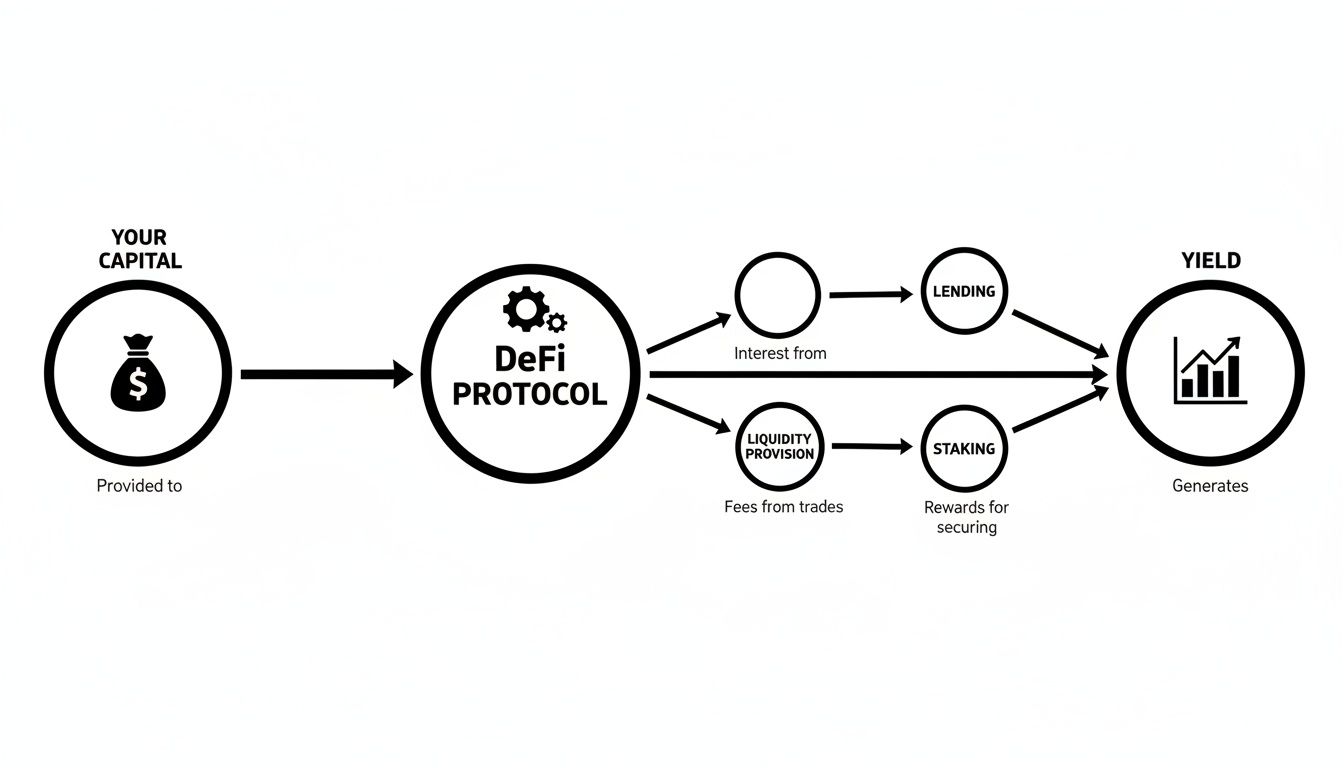

This diagram breaks down the basic flow of how your capital gets put to work to earn that yield in the first place.

The process is simple but incredibly powerful: you deposit your capital into a DeFi protocol, and it gets put to work in activities like lending or providing liquidity, generating a return. This cycle is the engine behind every bit of interest you earn on your stables.

The Challenge For Individual Investors

These constant market swings create a real headache for anyone trying to manage their funds by hand. The DeFi world is incredibly fragmented, with hundreds of protocols spread across dozens of blockchains, all offering different rates that can change by the hour.

The core challenge for a manual investor is the sheer effort required. You must constantly research, compare rates, assess risks, and pay transaction fees to move your funds from one protocol to another just to chase a slightly better APY.

This manual "yield farming" can quickly turn into a full-time job. It’s a grind that involves:

Continuous Monitoring: Trying to keep tabs on APYs across countless platforms like Aave, Compound, and a sea of decentralized exchanges.

Risk Assessment: Vetting the smart contract security and economic model of every new protocol that pops onto your radar.

High Transaction Costs: Burning cash on gas fees for every deposit, withdrawal, and transfer. These fees can absolutely eat up your profits, especially if you're not working with a huge amount of capital.

This constant churn is not just a time sink; it’s expensive and full of risk. For a better sense of the current market trends and the overall health of the ecosystem, you can check out the latest Defi statistics.

This is precisely the problem that smart, automated platforms are built to solve. They do the heavy lifting of navigating the yield landscape for you, making sure your capital is always working as hard as possible without the manual grind.

Understanding the Real Risks of Stablecoin Yielding

Those juicy yields you see from DeFi stablecoin interest don't just appear out of nowhere. They're your reward for taking on a few specific risks that you just don't find in traditional banking.

Knowing what you're up against isn't meant to scare you off. It's about going in with your eyes open so you can make smart moves with your money. Frankly, a no-nonsense breakdown of the threats is the best way to build real confidence.

Let's break down the main risks into three big buckets.

Smart Contract Risk

Think of a DeFi protocol like a high-tech vault that’s run entirely by computer code. Smart contract risk is the danger that someone finds a flaw in that code—a bug or a backdoor. Just like a physical vault might have a weak spot a locksmith could exploit, a smart contract can have a vulnerability a hacker can use to drain the funds.

We’ve seen it happen. Even big, reputable protocols have been hit by clever attackers who found a loophole in the code, and poof, the money was gone. This is probably the most direct and common risk in the DeFi world.

A protocol's code is its law, and if that law has loopholes, they can be exploited. This is why thorough, independent security audits are non-negotiable for any protocol you consider using.

Stablecoin De-peg Risk

This one is fundamental and tied to the very asset you're holding. Stablecoin de-peg risk is the chance your stablecoin stops being, well, stable. A stablecoin is only worth $1 because everyone believes it's worth $1, and that belief is backed by reserves and market confidence.

If something spooks the market, people might rush for the exits, trying to sell all at once. This can cause the price to "de-peg" and fall below a dollar. Imagine you’re holding 10,000 USDC and it suddenly de-pegs to $0.90. Your capital just took a $1,000 hit, which can easily wipe out months of earned interest.

Protocol Risk

This goes beyond just the code. Protocol risk is about the economic design, the governance, and the overall health of the entire platform. A few things fall into this category:

Flawed Tokenomics: The protocol might have an economic model that looks great on paper but is unsustainable long-term and could collapse under pressure.

Centralization Hotspots: If a small group of insiders holds all the keys, they could make bad—or even malicious—decisions that affect everyone.

Governance Gridlock: The community in charge of voting on changes might approve something harmful or, just as bad, fail to act quickly enough to stop a threat.

A protocol can have flawless code but still go under if its economic engine is built on shaky ground. It’s a subtle risk, but just as real. If you want to go deeper, we've got a full guide on understanding stablecoin risks and how to spot them.

At the end of the day, managing these risks boils down to two things: diversification and picking platforms built with security in mind from day one. Spreading your capital across several solid, well-audited protocols is always a better bet than putting all your eggs in one basket. That way, a single bug or de-peg event won't take down your whole strategy.

All the theory is great, but seeing how this actually plays out with real money is where it all clicks. Let's walk through a couple of practical examples to show how your stablecoins can start generating returns in DeFi.

We'll look at two of the most common jobs you can give your stablecoins: being a lender or a liquidity provider. Each one puts your capital to work in a slightly different way, but they're both fundamental to how this whole decentralized economy ticks.

Example 1: The Lender

First up, meet Alex. Alex has $5,000 in USDC sitting in a wallet, not doing much besides collecting digital dust. Instead of letting it sit idle, Alex decides to lend it out on a major DeFi protocol like Aave. Right now, the protocol is offering a respectable 5% APY for USDC lenders.

Let's do some quick back-of-the-napkin math on what that looks like:

Initial Capital: $5,000 USDC

Stated APY: 5.0%

Assuming that rate holds steady, we can figure out the earnings.

Annual Earnings Calculation: $5,000 * 0.05 = $250 per year

Daily Earnings Calculation: $250 / 365 days = ~$0.68 per day

Okay, so $0.68 a day isn't going to buy a Lambo. But it's completely passive income from capital that was previously earning zero. The real magic is that this yield is generated 24/7, compounding as it goes and showing you the simple power of putting your assets into a productive system.

Example 2: The Liquidity Provider

Now let's switch gears and look at another path. Taylor has $10,000 in USDC and wants to earn by helping a decentralized exchange (DEX) like Uniswap function. Taylor decides to become a liquidity provider (LP) by adding that capital to a popular USDC-DAI stablecoin pool.

Here, the earnings don't come from borrowers. Instead, Taylor gets a tiny slice of the fees from every single trade that happens in that pool. The yield is driven by trading volume, not lending demand.

Let's say the pool is busy enough that the trading fees add up to a 4% APY for liquidity providers.

Annual Earnings Calculation: $10,000 * 0.04 = $400 per year

These fees just stack up with every swap, turning market activity directly into returns for LPs like Taylor. It’s a perfect example of earning by providing the basic plumbing that makes the market work.

Grounding This in Reality

These examples use nice, clean percentages, but in the real world, DeFi yields are constantly in motion. They can swing pretty wildly based on what’s happening in the market. The stablecoin ecosystem is the engine of DeFi, with a cumulative total recently topping $120 billion, and giants like USDT and USDC dominate the space. On-chain data shows USDT can see average deposits of $34 million per period, while yields for popular stablecoins like USDC can spike to 20% or more when demand is high. You can dive deeper into the data behind DeFi activity on the Amberdata blog.

This is exactly why you need to keep your eyes open. The rate on one protocol might be 3%, while another is offering 7% for the very same stablecoin.

The key takeaway is that the opportunity is not uniform. Your potential DeFi stablecoin interest depends heavily on the specific stablecoin, the protocol you choose, and overall market conditions at that moment.

To give you a clearer picture of this diversity, check out this hypothetical snapshot of what you might find across the DeFi landscape.

Example Stablecoin Interest Rates Across DeFi (Hypothetical)

This table shows the kind of annual percentage yields (APYs) you could expect for different stablecoins across various DeFi protocols. It’s not fixed, but it gives you a good feel for the range of possibilities.

Stablecoin | Protocol Type | Example APY Range |

|---|---|---|

USDC | Lending Protocol (e.g., Aave) | 3% - 8% |

USDT | Liquidity Pool (e.g., Uniswap) | 2% - 6% |

DAI | Yield Aggregator | 4% - 12% |

PYUSD | Lending Protocol | 5% - 10% |

As you can see, someone holding DAI might get a better rate from a yield aggregator, whereas a USDC holder might stick to a blue-chip lending protocol. These simple actions—lending your assets or providing liquidity—are what make the multi-billion dollar DeFi world go 'round, and they offer a clear path for your capital to get in on the action.

Automating Your Strategy with AI and Yield Seeker

Let's be honest: manually chasing the best stablecoin interest rates in DeFi is a total grind. You're constantly jumping between protocols and chains, trying to figure out which one has the best APY today. Then you have to weigh the smart contract risks, pay gas fees for every move, and do it all over again next week when the rates change.

What starts as a cool way to earn passive income quickly turns into a full-time job. It's just not sustainable for most people.

But what if you could get those top-tier returns without all the manual legwork? This is exactly where smart automation comes in, and it's a complete game-changer for how you can earn in DeFi.

Let an AI Agent Do the Heavy Lifting

Think about having a personal crypto analyst working for you 24/7, with just one job: find the best risk-adjusted yield for your stablecoins. That’s pretty much the whole idea behind Yield Seeker. Instead of you doing all the research, our platform gives you a personalized AI Agent to handle everything.

Your agent is always scanning a curated list of pre-vetted DeFi protocols. It’s not just blindly chasing the highest number; it’s smarter than that. It weighs the potential return against a deep analysis of a protocol's security, its track record, and what's happening in the market right now.

When your agent spots a better opportunity that fits your strategy, it can automatically move your funds to keep you in the optimal position, maximizing what you earn.

This approach knocks out the three biggest headaches of manual yield farming:

Constant Research: The AI does the market watching, so you don’t have to.

Complex Risk Analysis: The agent only operates within a secure ecosystem of protocols we’ve already vetted.

Costly Transactions: By making smart, optimized moves, it keeps gas fees from eating into your profits.

Effortless Yield for Everyone

We built Yield Seeker to make earning solid DeFi interest simple, no matter how much you know about crypto. We've stripped away all the friction so you can just focus on the results.

Our mission is to give you back your time while growing your capital. By automating the complex decision-making, Yield Seeker becomes your smart partner, navigating the DeFi maze for you. The goal is to let you earn more with way less effort.

Here’s a peek at the Yield Seeker dashboard. We designed it to give you a clean, at-a-glance view of your strategy in action.

The interface makes it dead simple to track your total balance, watch your earnings grow in real-time, and see exactly how your AI Agent is putting your funds to work.

The benefits are obvious, especially if you want the upside of DeFi without the day-to-day grind.

Key Advantages of Using Yield Seeker

True Automation: Set up your strategy once, and the AI Agent takes it from there. It constantly rebalances to keep you in the most optimal spots.

Low Barrier to Entry: You can get started with as little as $10 in USDC. This makes it easy to kick the tires and see how it works without a big commitment.

Complete Flexibility: Your funds are never locked. You can deposit or withdraw your capital anytime you want, giving you total control.

Full Transparency: From a single dashboard, you can see exactly where your funds are and how your returns are being generated. No black boxes.

If you're curious about the tech behind this, we dig into a lot of these ideas in our article on how to use AI for investing.

Ultimately, by handing off the repetitive, analytical tasks to a capable AI, you can tap into the world of DeFi stablecoin yields without needing to be an expert yourself.

Alright, you've got the basics down. But I know what it's like—the more you learn about DeFi, the more questions pop up.

Let's tackle some of the common ones that people have before they're ready to jump in.

Is Earning Interest on Stablecoins Safe?

Look, nothing in life—or in crypto—is 100% risk-free. Anyone who tells you otherwise is selling something.

But earning yield on stablecoins through well-known, audited DeFi protocols is about as safe as it gets in this space. The real trick is managing that risk. You wouldn't put all your money in one stock, and you shouldn't put all your crypto in one protocol. Diversifying is key.

This is where automation is a game-changer. An AI-driven platform like Yield Seeker can spread your funds across a pre-vetted list of opportunities automatically. It helps you dodge those single points of failure that can really sting manual investors.

How Much Can I Realistically Earn from Stablecoin Interest?

This is the million-dollar question, and the honest answer is: it depends. The market is always moving.

When there’s a lot of borrowing demand in DeFi, you can see APYs jump up to 10-20%, sometimes even higher. In quieter times, things might cool down to the 3-7% range. Even then, that’s way better than what your bank is offering.

The real edge of an automated strategy is that it doesn't just sit there. It’s always hunting for the best risk-adjusted rate for your DeFi stablecoin interest, moving funds in real-time so you're not leaving money on the table. All without you having to lift a finger.

Do I Need to Be a DeFi Expert to Get Started?

Absolutely not. While it helps to understand what's going on under the hood (which is why you're reading this!), modern tools are built for everyone.

You don't need to be a full-time degen or analyst anymore. Platforms like Yield Seeker are designed to handle all the complicated stuff—the transactions, the protocol-hopping, the risk assessment—behind a simple interface.

You get all the benefits of DeFi yield without having to become an expert yourself. You can literally start earning passive income in a few minutes.

Ready to put your stablecoins to work effortlessly? Yield Seeker uses a personalized AI Agent to find and manage the best risk-adjusted yields for you. Start earning smarter today.