If you're holding stablecoins right now, you're probably facing a familiar problem. Lending rates move, liquidity mining comes and goes, and every app claims to offer a cleaner route to passive yield than the last one. The hard part isn't finding opportunities. It's understanding what powers them, what can erode your returns, and which strategies can be left alone versus which ones demand active management.

At the center of that mess sits the amm, short for automated market maker. If you've swapped tokens onchain, deposited into a stablecoin pool, or chased fee income from liquidity provision, you've already used one. Users generally interact with AMMs without thinking much about them. That's fine until execution quality, slippage, or pool design starts deciding whether your yield is real or just theoretical.

For stablecoin holders, AMMs matter because they turn idle capital into trading liquidity. Traders use that liquidity to swap. Liquidity providers collect fees. That basic loop is one of the core engines of DeFi yield. But the details matter a lot more than beginner guides usually admit.

The Unseen Engine of Decentralized Finance

Traditional markets usually rely on an order book. Buyers post bids. Sellers post asks. A matching engine pairs them off. That works well when you have market makers, centralized infrastructure, and a venue coordinating everything.

DeFi needed a different model. Onchain trading couldn't depend on a single operator standing in the middle or on users waiting around for a matching counterparty. The solution was the AMM. Instead of matching people directly, the protocol lets users trade against a pool of assets governed by code.

A good mental model is a vending machine with dynamic pricing. You don't negotiate with another person. You put one asset in, take another asset out, and the machine recalculates the next price based on what's left inside.

That design solved a real coordination problem. It made continuous onchain liquidity possible for assets that otherwise would've traded poorly or not at all. By the start of 2026, AMMs on major chains like Ethereum and Base collectively held over $50 billion in total value locked, acting as a primary liquidity layer for modern onchain finance, according to DeFiLlama's tracked TVL data.

Why AMMs matter for stablecoin yield

For a stablecoin holder, the AMM isn't just a trading venue. It's a cash-flow machine when used well. You deposit capital into a pool, traders pay fees to use that pool, and your position earns part of those fees.

The catch is that not all pools behave the same way. A volatile pair and a stablecoin pair can both be called AMMs, but the risk profile is completely different. That's why it helps to understand how liquidity pools work in practice, not just in theory.

Where builders focus in the real world

Teams building exchanges don't treat AMMs as a toy formula anymore. They think about routing, pricing, liquidity concentration, and execution under stress. If you're curious how this gets translated into actual products, a DEX development company can be a useful reference point because it shows how much engineering sits underneath the simple front-end swap box.

Practical rule: If a yield opportunity depends on an AMM, don't stop at the headline APY. Ask what pool design is underneath it, who trades there, and what your realized exit price is likely to be.

How AMMs Create Prices with Simple Math

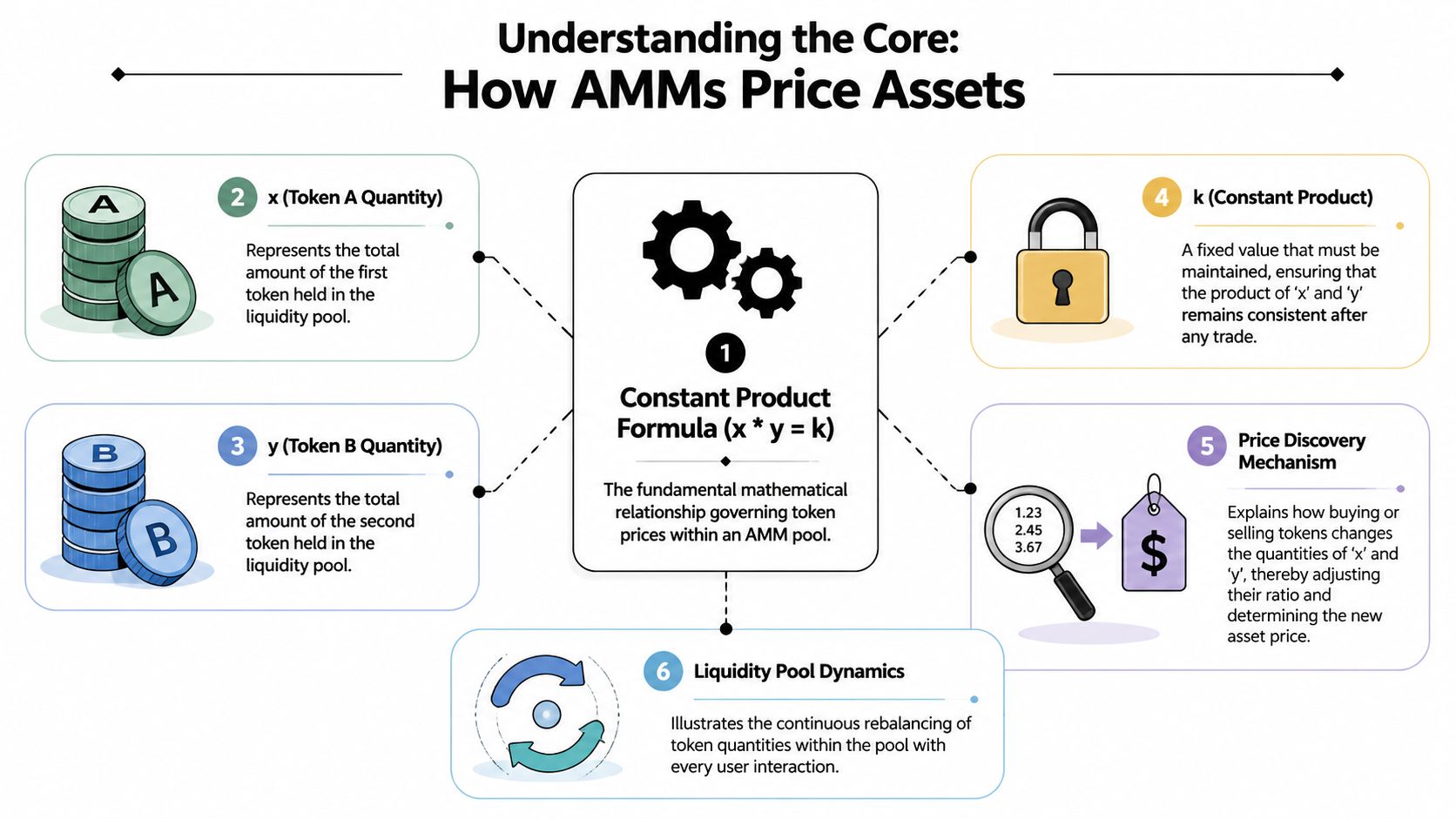

The classic AMM model uses a simple rule: x * y = k.

You don't need to love formulas to understand it. Treat it like a balance that always has to preserve a product. If one side goes down because a trader removes tokens, the other side has to go up enough to keep the equation intact. That's what causes the price to move during a swap.

A simple pool example

Say a pool starts with:

10 ETH

20,000 USDC

The implied starting price is 2,000 USDC per ETH because the pool holds 20,000 USDC against 10 ETH.

The constant product is:

10 × 20,000 = 200,000

Now a trader comes in and buys ETH with USDC. They add USDC to the pool and remove ETH from it. After the trade, the product still has to stay at 200,000, but the token balances will be different.

If the trader removes some ETH, the pool has less ETH available. That makes each remaining ETH more expensive. The next buyer gets a worse price than the previous one. That's the whole mechanism in plain English.

Why bigger trades move price more

New users are often surprised by this dynamic. An AMM doesn't quote one fixed market price for any trade size. It gives you a path through the curve. Small trades touch only a little of that curve. Large trades push much further along it.

That means two things:

Pool depth matters. Deeper pools absorb trades better.

Execution quality matters. The price you expected and the price you got can differ meaningfully.

If you want a more focused breakdown, this guide on what slippage means in trading is worth reading before you LP or swap size through any pool.

Think of a constant-product AMM as a bowl. A small marble barely changes the waterline. A heavy stone changes it fast.

What the formula gets right and where it struggles

The constant product model is elegant because it's simple, permissionless, and always available. It doesn't need a market maker manually updating quotes. It lets liquidity sit onchain and serve traders continuously.

Its weakness is also obvious once you've used it enough. It can be capital-inefficient. If most trading happens near one price, spreading liquidity across a huge range wastes a lot of capital. That's why newer AMM designs exist.

A Tour of Major AMM Designs

AMM is a category, not a single design. Different models exist because different trading problems need different liquidity curves.

The easiest way to think about it is this. The original constant-product AMM was the durable first version. Later models specialized. Some got better at stablecoin swaps. Some got better at multi-asset exposure. Some improved capital efficiency but demanded more active management.

The main families

Constant Product Market Maker

This is the classic Uniswap-style design. It works well for general token pairs and remains the easiest AMM model to understand. The downside is that a lot of liquidity sits far away from the price where trades happen.

StableSwap

Curve popularized this design for assets that should trade close to one another, such as stablecoins. That's why it became central to stablecoin liquidity. Stablecoin pools like Curve's 3pool often process hundreds of millions of dollars in daily volume while keeping slippage for a $1 million trade under 0.05%, according to Curve's pool research pages. A plain constant-product pool would struggle to match that kind of efficiency for same-priced assets.

Weighted pools

Balancer-style pools let you hold more than two assets with custom weights. That makes them useful when you want one pool to behave more like an index or treasury basket than a simple swap pair.

Concentrated liquidity

Uniswap v3 made liquidity far more capital-efficient by letting LPs choose a price range instead of providing liquidity everywhere. This can improve fee generation when your range is well placed. It also means your position needs more attention. If price moves outside your chosen band, your capital can stop earning trading fees until you reposition it.

Comparison of Common AMM Types

AMM Type | Core Formula Principle | Best For | Key Trade-off |

|---|---|---|---|

Constant Product | Keeps token product constant as reserves change | General token pairs | Simple, but less capital-efficient |

StableSwap | Uses a curve designed for similarly priced assets | Stablecoin swaps and wrapped assets | Great execution near parity, weaker fit for volatile pairs |

Weighted Pool | Maintains preset asset weights across a basket | Treasury-style or index-like exposure | More moving parts, not ideal for every swap route |

Concentrated Liquidity | Liquidity is placed inside selected price ranges | Active LP strategies and high-efficiency pairs | Higher maintenance and range risk |

What works for stablecoin users

For stablecoin yield, StableSwap-style pools usually make the most intuitive sense. They aim to preserve tight execution around assets that should trade near par, which is exactly what stablecoin users want.

Concentrated liquidity can also work well for stablecoin pairs, especially when the market spends long stretches inside a narrow band. But that approach rewards attention. Passive capital often becomes unproductive if the range is off.

A lot of people choose an AMM like they're choosing a brand. The better question is whether the curve matches the job.

What doesn't work as well

A volatile-token AMM can advertise a strong fee stream and still be a poor fit for someone parking treasury cash or reserve stablecoins. The fee line might look attractive, but the path to realizing that yield can be messy if price swings, depth disappears, or exits get expensive.

That's the practical dividing line. For stablecoin capital, the ideal AMM isn't the most exciting one. It's the one that delivers predictable execution and durable fee generation without forcing constant intervention.

The Unspoken Risks of AMM Liquidity

Most AMM explainers obsess over impermanent loss. That's a real risk, but it isn't the only one, and for many users it isn't even the first one they feel.

What hits faster is execution. You enter a pool expecting to earn fees, then discover that swaps cost more than expected, exits move the market, or MEV bots take a cut from your transaction quality.

Impermanent loss is real, but it's not the whole story

Impermanent loss is easier to understand if you stop treating it like a mysterious DeFi tax. It's the gap between holding assets in a pool versus holding them in your wallet while their relative prices change.

With stablecoin pools, that risk is usually framed as lower because the assets are meant to stay close in value. That's often true in normal conditions. It becomes less comforting when one stablecoin depegs, liquidity thins out, or the market suddenly treats two "stable" assets very differently. If you want a clean explanation before taking LP exposure, read this breakdown of impermanent loss and why it happens.

The risks traders feel immediately

The more common operational risks look like this:

Slippage: Your trade clears at a worse average price than the quote suggested.

Gas and fees: A strategy that looks profitable before execution can look mediocre after costs.

MEV exposure: Searchers and bots can exploit visible transaction flow.

The Bank for International Settlements notes that AMM bonding curves can expose liquidity providers to impermanent loss and make traders more likely to avoid AMMs because they may be front-run. It also states that transparent AMM pricing makes sandwich attacks structurally possible, which can threaten DeFi's long-term viability, according to the BIS quarterly review on DeFi and AMMs.

That matters because sandwich attacks aren't a niche corner case. They are a structural side effect of broadcasting intent into a transparent system where bots can react before and after your trade settles.

What a sandwich attack looks like in practice

A bot sees your pending swap.

It buys ahead of you.

Your trade executes at a worse price.

The bot sells after you and captures the difference.

You don't need to be making a massive trade to care. You just need to care about realized execution instead of quoted execution.

Here's a visual explainer that does a good job showing where that damage comes from:

What actually helps

There isn't one universal fix, but a few habits reduce avoidable damage:

Use deeper pools. Stablecoin pairs with heavy routing and proven liquidity usually produce cleaner fills.

Avoid forcing size through thin venues. A yield edge can disappear on entry or exit.

Be careful with manual slippage settings. Tight settings can cause failed transactions. Loose settings can invite bad execution.

Treat APR screenshots skeptically. A fee number without execution context is incomplete.

Don't evaluate an AMM position only by the yield you collect. Evaluate the all-in round trip of entering, sitting in the pool, and exiting under pressure.

For stablecoin users, this section is where AMMs stop being abstract. The main question isn't "can this pool earn fees?" It usually can. The actual question is whether those fees survive contact with actual market conditions.

Using AMMs to Earn Stablecoin Yield

The basic income model is simple. You provide liquidity to a pool. Traders pay fees when they swap through it. The protocol distributes a share of those fees to liquidity providers.

That works best when three conditions hold at the same time: the pair is heavily traded, the pool is deep enough to keep execution attractive, and the asset mix doesn't introduce more risk than the fees can justify. Stablecoin pools are popular because they often meet those conditions better than volatile token pairs.

Where the yield comes from

For a stablecoin LP, fee income is the first place to look. In 2025, top-tier stablecoin liquidity providers could earn between 5% to 15% APY from trading fees alone, before additional token incentives, according to Token Terminal's protocol analytics platform.

That range is useful because it frames AMM yield the right way. Good pools don't need a giant emissions story to make sense. Trading demand itself can produce meaningful return.

A practical way to think about fee APY

You don't need a perfect spreadsheet model to evaluate a pool. Start with a few questions:

Does this pool have real swap demand? Fee income only exists if traders use the venue.

How crowded is the liquidity? More liquidity can mean safer execution but lower fee share per dollar deposited.

Is the pool design appropriate for the assets? Stablecoins belong in stablecoin-optimized designs more often than not.

A rough mental model works like this. If a pool attracts steady volume and charges fees on each swap, your return depends on what portion of the pool you own and how much of those fees flow to LPs. If volume rises while total liquidity stays manageable, your fee yield improves. If liquidity floods in faster than volume, your slice of fee income gets diluted.

What works versus what doesn't

What tends to work:

Stablecoin pairs with organic volume

Pools used by aggregators and repeat flow

Setups where fee income stands on its own

What often disappoints:

Pools that rely mostly on temporary token rewards

Pairs with unstable "stable" assets

Strategies where entry and exit costs erase the carry

If you want to compare LP reward mechanics in a prediction-market context, this Guide for Polymarket LP traders is a useful example of how venue design changes the economics of providing liquidity.

Operator mindset: Fee yield is stronger than incentive yield. Incentives can help. They shouldn't be the whole thesis.

The Future Is Automated AMM Management

You deposit stablecoins into a pool on Monday because the fee profile looks attractive. By Friday, volume has shifted, liquidity has crowded in, your position is less efficient, and a rebalance now has to clear gas costs, slippage, and MEV risk. That is the operating reality for modern LPs. AMM participation has become a software problem.

AMMs began by automating trade execution. The next step is automating capital management for LPs. That shift is already underway. Tools such as Consensys' Gamma Strategies handle concentrated-liquidity maintenance, fee reinvestment, and range updates without requiring users to babysit positions, a pattern also noted in Binance Square's overview of evolving AMM structure.

Why manual management breaks down

Manual LPing still works for simple positions on a single venue. It breaks down once capital is spread across chains, pool designs, and changing market conditions.

The workload is not just analytical. It is operational. Someone has to watch whether fees still justify the capital, whether the pool is attracting organic flow or just temporary mercenary liquidity, whether a concentrated range is drifting out of usefulness, and whether reallocation costs wipe out the gain from moving. Stablecoin strategies make this more subtle, not less, because the headline volatility is lower while the execution drag can still be meaningful.

That is where many yield projections fall apart in practice. A pool can look attractive on a dashboard and still produce mediocre net results after timing mistakes, poor range management, and expensive repositioning.

Where AI-driven tools fit

AI is useful here for process discipline, not prophecy. The best use case is continuous monitoring across fragmented markets, then ranking opportunities with the same constraints an experienced operator would care about: net yield after costs, liquidity crowding, pool design, venue quality, and the chance that execution itself will erode the edge.

For busy treasury teams and stablecoin holders, that matters more than another dashboard. Good automation can flag when a position no longer earns enough, suggest whether to stay put or rotate, and reduce the manual overhead of comparing pools that look similar on the surface but behave very differently once slippage and MEV enter the picture.

Yield Seeker fits into that category. The product uses AI-driven monitoring and allocation logic to help manage stablecoin capital across DeFi strategies, which is a better match for users who want AMM yield exposure without turning pool management into a full-time job.

The practical takeaway is simple. AMMs will keep generating opportunities, but the edge is shifting from access to execution. For stablecoin yield, the next wave is not a new invariant. It is better automation around selection, monitoring, and reallocation.