If you're holding stablecoins right now, you're probably in a familiar spot. You want yield, but you don't want to spend your evenings comparing pools, checking dashboards, and wondering whether a decent-looking return is concealing ugly risk.

That tension is where automated market makers, or AMMs, matter. They aren't just a DeFi buzzword. They are one of the core mechanisms that made decentralized trading possible in the first place, and they sit underneath many of the yield opportunities stablecoin holders see today.

The tricky part is that AMMs look simple from the outside. Deposit assets, earn fees, maybe collect incentives. But once your money is in the pool, the math, trading flow, and design choices start shaping your real outcome. Slippage changes execution. Pool design changes risk. Arbitrage keeps prices aligned. And if you're trying to earn yield on stablecoins, those mechanics become your daily reality whether you understand them or not.

The Dawn of Decentralized Trading

You hold USDC and want to swap into another stablecoin before a payment goes out, or move into ETH after a market dip. On a traditional exchange, that trade depends on someone on the other side posting the right order at the right time. Onchain, that dependency was a serious bottleneck.

Early decentralized trading had a simple problem. Order books work well when an exchange can coordinate market makers, custody assets, and keep matching engines running offchain. Blockchains are slower, transparent, and expensive to update one order at a time. A system built for nonstop onchain trading needed a different way to find liquidity.

AMMs provided that shift. Instead of waiting for a buyer and seller to meet, traders swap against assets already deposited in a smart contract. The pool becomes the standing inventory for the market.

If you're new to the pool side of this system, this primer on how liquidity pools work in DeFi is a useful starting point.

Why this changed DeFi

The practical effect was bigger than the mechanism itself. AMMs turned trading into something blockchains could support continuously, with prices updating from pool balances and fees flowing back to the people who supplied the assets.

That changed three things at once:

Access opened up. Anyone with a wallet could trade through a smart contract.

Liquidity became a product. Instead of only traders participating, depositors could supply assets and earn fees.

New markets could appear quickly. A pool could be launched without relying on a centralized exchange to list the pair.

That last point matters for stablecoin holders more than it first appears. Stablecoin yield in DeFi often starts with a simple question: where does the cash flow come from? In many cases, it comes from swap activity. Traders moving between USDC, USDT, DAI, FRAX, or from stablecoins into volatile assets, pay fees to use that pooled liquidity.

AMMs turned idle stablecoins into working inventory. Your dollars, or dollar proxies, can sit in a pool like chips at a cashier's window. Each trader who comes through pays a small toll for access to that inventory. The opportunity is obvious. The harder part is that not every toll booth earns the same amount, and not every pool exposes you to the same risk.

That is the core setup for yield optimization. A stablecoin holder is not only choosing "where APY looks highest." They are choosing a market structure, a fee stream, a slippage profile, and a risk package. Platforms like Yield Seeker exist because those choices are hard to evaluate by eye, especially when conditions change pool by pool and hour by hour.

AMMs mattered because they made decentralized trading usable. For anyone earning on stablecoins, they also created a constant allocation problem: which pools are paying enough to justify the mechanics underneath them.

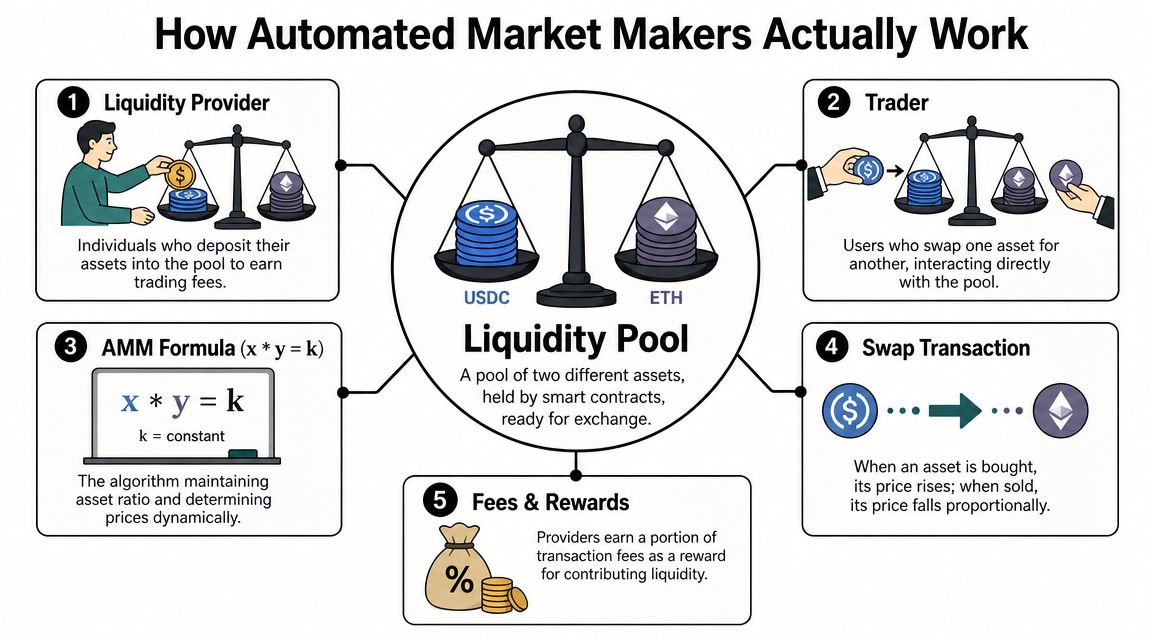

How Automated Market Makers Actually Work

You deposit USDC into a pool because the fee yield looks attractive. An hour later, traders have swapped heavily against that pool, the token balances have shifted, and the price inside the pool is no longer where it started. That is the first mental model to get right. An AMM is not a savings account. It is a pricing machine that uses your capital as inventory.

The pool is the counterparty

On a traditional exchange, a buyer and seller meet through an order book. In an AMM, the trader faces a pool of assets held in a smart contract.

Those assets come from liquidity providers, or LPs. They deposit tokens into the contract, and the contract applies a formula to decide the swap price after each trade. If you want the pool mechanics from the LP side, this guide on what liquidity pools are fills in that part well.

The flow is straightforward:

An LP deposits two assets into a pool.

A trader sends in one asset and takes out the other.

The pool's reserves change.

The AMM formula recalculates the price from the new reserve balance.

The trader pays a fee, and that fee goes to LPs based on the pool's rules.

That last step is why stablecoin holders care. The yield does not appear by magic. It comes from people paying to trade against the inventory you supplied.

The famous x times y equals k rule

The best-known AMM design is the constant product model, written as x * y = k.

Here, x represents the amount of one asset in the pool, and y represents the amount of the other. The pool tries to keep the product of those two reserve balances in line with the rule. If a trader removes ETH, they must add enough USDC so the new reserve state fits the formula.

You do not need much algebra to see what this does in practice. As one side of the pool gets scarcer, buying more of it becomes progressively more expensive. The curve has built-in resistance. A small trade nudges the price. A large trade pushes much harder.

A grocery shelf is a useful analogy. If there are plenty of cartons left, taking one does not change much. If only a few remain, each additional carton taken matters more. In an AMM, reserve depth plays the same role.

Why each swap changes the next price

Suppose a USDC-ETH pool starts with balanced reserves. A trader buys ETH using USDC. After the trade, the pool holds more USDC and less ETH.

That new reserve ratio implies a new price.

The next trader now faces a pool where ETH is scarcer than it was one trade ago, so the next unit of ETH costs more. This is why AMMs quote prices continuously without an order book. The reserves are the quote.

For stablecoin pairs, the same logic applies, but the movement is usually tighter because both assets are designed to stay near one dollar. That makes pools like USDC-USDT appealing for treasury cash, idle balances, and conservative LP strategies. It also explains why stablecoin holders spend so much time comparing pool depth, fee rates, and trading volume. Small differences in structure can change net yield in a meaningful way.

If you want a plain-language definition of price movement during execution, What is slippage gives the trading term that shows up every time a pool reprices during a swap.

What this means for yield

For a stablecoin holder, the practical question is not only "does this pool pay fees?" The better question is "what kind of trading engine am I funding, and how does that engine convert flow into yield?"

A quiet pool may expose you to limited price movement but produce little fee income. A busy pool may generate stronger cash flow, but the same trading activity can shift balances, attract arbitrage, and change your risk profile. That is why AMM mechanics matter so much for yield optimization. The formula, the reserve depth, and the type of assets in the pool all shape the return you keep.

This is also where tools like Yield Seeker become useful in a practical, non-theoretical way. Stablecoin allocation is a live market selection problem. You are comparing fee streams, pool behavior, and execution conditions that can change throughout the day, not just chasing the highest posted APY.

The Key Tradeoffs Slippage Impermanent Loss and Fees

Once you understand that an AMM is a live trading engine, the next question is obvious. What's the catch?

For most users, three forces matter most: slippage, impermanent loss, and fees. They pull in different directions, and your real result depends on how they interact.

Slippage is the execution cost you feel first

Slippage is the gap between the price you expected and the price you received. In AMMs, that happens because the trade itself moves the pool.

Binance Academy explains it plainly in its AMM overview. Larger trades move the pool price more, so slippage rises as trade size grows relative to pool depth. That's why deep pools matter so much for stablecoin strategies.

If you want a clean glossary-style definition before going deeper, Finzer's explainer on what slippage means in trading is a useful reference.

A simple way to understand this:

Trade setup | Likely outcome |

|---|---|

Small swap in a deep stablecoin pool | Lower price impact |

Large swap in a shallow pool | Higher price impact |

Repeated treasury rebalances through thin liquidity | Execution quality deteriorates fast |

For stablecoin holders, this isn't abstract. If you're rotating between pools or reallocating capital regularly, slippage can erode yield.

Impermanent loss is a comparison problem

Impermanent loss confuses people because it isn't a fee charged to you. It's the difference between two worlds:

You provided liquidity

You just held the assets

If the relative prices of the pooled assets move, the AMM keeps rebalancing your position. When you later withdraw, you may end up with a different mix than you started with. That mix can be worth less than holding the original assets outside the pool.

The loss is called "impermanent" because if prices return to the original ratio, the gap can narrow. But for many users, that label creates false comfort. The moment you withdraw, the result becomes real.

If you want the mechanics broken down in more detail, this explainer on impermanent loss is worth reading.

In volatile pairs, LPs are often selling relative winners and buying relative losers automatically. That's the mechanism behind impermanent loss.

For stablecoin pools, impermanent loss can look different from what you see in volatile token pairs. If the assets stay closely aligned, the effect may be milder. But if one stablecoin depegs or market stress widens the gap between "similar" assets, the risk picture changes quickly.

Fees are the reason LPs show up

AMMs need liquidity providers, so pools typically share swap fees with them. That fee flow is the economic incentive that keeps capital in the system.

The challenge is that fee income isn't free money. It has to compensate for the risks and frictions sitting underneath the pool.

A practical LP checklist looks like this:

Trading activity matters. No volume means little fee generation.

Pool depth matters. Better depth can improve execution and attract more usage.

Asset behavior matters. Stablecoin pools behave differently from volatile pairs.

Timing matters. A pool that looked attractive yesterday can become less appealing if liquidity, market structure, or token behavior shifts.

For stablecoin yield seekers, the primary question isn't "Does this pool pay fees?" It's "Do the fees outweigh the execution drag and portfolio risks I'm taking?"

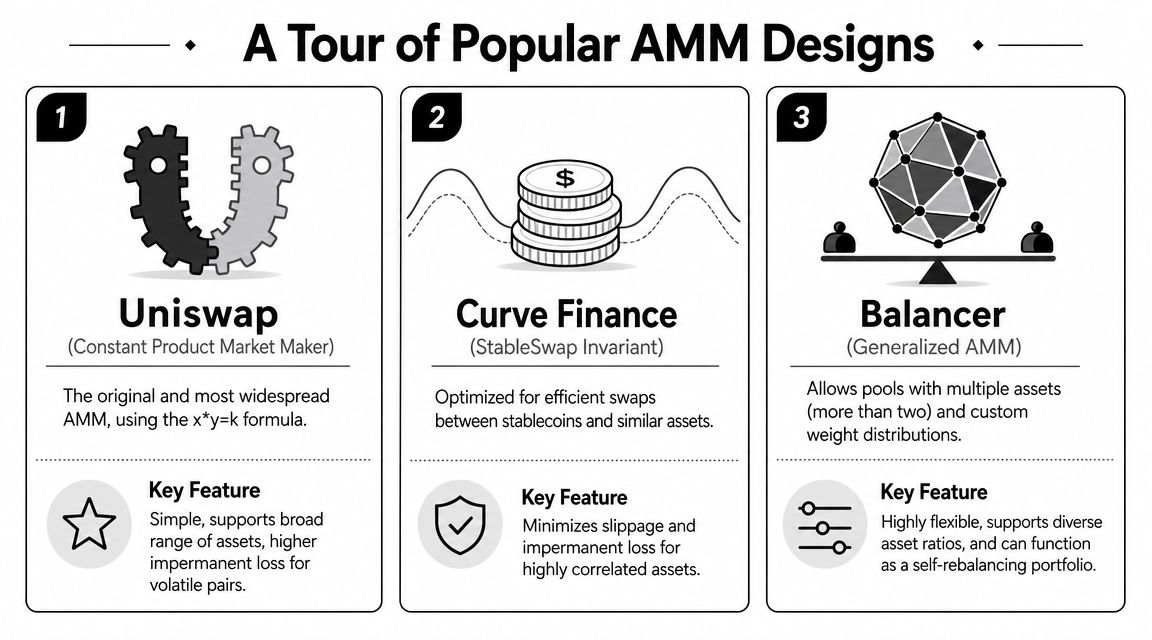

A Tour of Popular AMM Designs

A stablecoin holder comparing AMMs is making a market-structure decision, not just chasing the highest displayed yield.

Two pools can both quote an attractive APY and still behave very differently once real money starts moving through them. The reason sits under the interface, in the pricing curve, the assets the pool was built for, and the way liquidity is arranged. If you hold stablecoins, those design choices affect how much swap flow a pool attracts, how much slippage traders face, and whether fee income is likely to hold up under stress.

A useful way to frame AMM design is to compare them to different kinds of roads. Some are built to handle almost any traffic. Some are optimized for a narrow but common route. Some work more like a network of lanes with custom rules. All can move value onchain. They just do it with different strengths and different costs for LPs.

Uniswap and the general-purpose model

Uniswap popularized the broad, permissionless AMM template. Its constant product design works across many token pairs without needing those assets to stay close in price.

That flexibility is why it spread so quickly. A builder can launch a market for almost any pair, and a trader can often find liquidity without waiting for an exchange to list it.

For LPs, especially stablecoin holders, the practical takeaway is simple. A general-purpose pool is built for breadth first. If the pair is volatile or the liquidity is thin relative to order flow, price impact rises faster and the fee opportunity has to cover more strain.

Protocol style | Best fit | What stablecoin holders should watch |

|---|---|---|

Uniswap-style constant product | Broad token variety | Good general utility, but stablecoin yield can be less efficient than a specialist design |

Stable-asset specialist | Similar assets like stablecoins | Better execution near parity, but results depend on the assets actually staying close |

Multi-asset weighted pools | Portfolio-like baskets | More knobs to tune, which means more assumptions to monitor |

Curve and the specialist approach

Curve was built around a narrower question: what if the pool mostly serves assets that should trade near the same value, such as USDC, USDT, and DAI?

That focus changes the curve and the user experience. Near parity, the pool can offer trades with less friction than a general-purpose design, which makes it attractive for stablecoin routing and for LPs who want fee flow from stable-to-stable demand. A highway analogy fits here. Uniswap is a versatile road system. Curve is a high-capacity commuter line built for a route that gets repeated all day.

For stablecoin yield, this matters a lot. If your capital sits in assets that are supposed to stay close, a specialist AMM can turn that assumption into better trading conditions and, in many cases, a better fee-generation setup. But the word "supposed" matters. If one asset drifts, depegs, or becomes the token traders rush out of, the same design can concentrate the pool into the weaker asset faster than many depositors expect.

A stablecoin strategy works best when the pool design matches the actual behavior of the assets, not the label attached to them.

Balancer and the flexible portfolio model

Balancer approaches AMMs from another angle. Instead of centering everything on a simple 50/50 two-token pool, it supports multiple assets and custom weights.

That makes a pool feel less like a single market and more like a rules-based basket that traders can rebalance for you. If a pool holds 80% of one asset and 20% of another, every trade nudges it back toward those target weights. LPs collect fees while the pool maintains that structure.

For stablecoin holders, Balancer-style designs can be useful when yield strategy overlaps with portfolio construction. You may want stablecoins plus a smaller allocation to another asset, or a basket that reflects treasury preferences instead of a plain two-asset pair. The tradeoff is complexity. More assets and more custom parameters create more ways for a pool to behave differently from your initial assumption.

Why design choice matters for yield

Analysts at the Bank of Canada describe an "ecology of automated market makers" in their 2024 AMM research paper, emphasizing that protocols such as Uniswap, Curve, Sushiswap, and Balancer differ in design, governance, incentives, and risk.

That observation maps directly to the stablecoin yield problem. If two pools pay fees from different kinds of trade flow, use different curves, and react differently under pressure, they are not interchangeable income sources. They are different machines with different failure modes.

A disciplined stablecoin depositor should ask:

Are these assets expected to trade close together, or do they only look similar in calm markets?

Does the pricing curve match the kind of swap activity the pool gets?

Is the fee stream coming from repeat stablecoin routing, or from short-lived incentives that can disappear?

How much complexity am I accepting in exchange for the quoted yield?

Those questions are close to the systems mindset used in software engineering. Teams working on mitigating AI project risks study assumptions, failure modes, and changing conditions instead of trusting headline metrics. AMM selection deserves the same discipline.

For Yield Seeker's style of optimization, this is the core input. The job is not to find "an AMM" for stablecoins. The job is to identify which AMM design, on which chain, with which pool conditions, offers fee income that still makes sense after you account for execution quality, asset behavior, and the possibility that today's stable pool looks very different next week.

Real Risks Beyond the Basics

Most AMM explainers stop at impermanent loss. That's useful, but incomplete.

For depositors, especially stablecoin holders trying to earn yield, the deeper risk stack includes smart-contract risk, liquidity fragmentation, and MEV, including sandwiching. Those issues often matter just as much as the pricing curve itself.

Smart-contract risk is protocol risk

An AMM is software that holds and routes real capital. If the contract has a flaw, if an integration fails, or if governance introduces a bad change, users inherit that risk.

The useful mindset here comes from software engineering. Good teams don't just ask whether a system works in normal conditions. They ask how it fails, who can change it, and what controls exist around those changes. That same discipline shows up in broader discussions about mitigating AI project risks, and it's just as relevant when your yield depends on smart contracts.

A practical review should include:

Code exposure. How much capital and complexity sit inside the system?

Governance surface. Who can modify parameters or upgrade contracts?

Dependency chain. What other protocols, oracles, or bridges does the AMM rely on?

Liquidity fragmentation changes the real opportunity set

DeFi doesn't present one clean market. It spreads liquidity across many pools, chains, and fee tiers.

That fragmentation creates two problems for stablecoin holders. First, the "best" yield may be split across venues and hard to compare. Second, moving capital between venues introduces new costs and operational risk.

The result is that attractive-looking pools can be misleading in isolation. A strong nominal yield in a fragmented corner of the market may come with weaker execution, lower exit flexibility, or thinner liquidity when conditions change.

MEV is the invisible tax many users don't model

Maximal extractable value, or MEV, is one of the least understood AMM risks among newer users. In plain terms, bots can observe pending transactions and try to profit by inserting their own trades around yours.

A common example is the sandwich attack. If a bot sees your swap coming, it may trade before and after you, shifting the execution against you and capturing profit from the move.

The broader research point is that beginner content often misses this risk stack. The article source provided in your brief notes that AMM depositors need to think beyond impermanent loss and account for smart-contract risk, liquidity fragmentation, and MEV, while also noting that platforms like Uniswap, Curve, and Balancer have materially different designs, governance, incentives, and risks, discussed in the cited INFORMS publication.

If two pools advertise similar yield, the safer choice may be the one with cleaner execution, simpler dependencies, and more resilient liquidity.

That is why stablecoin yield isn't just a hunt for the highest number on the screen. It's a risk selection problem.

Optimizing Stablecoin Yield with AMMs and AI

Stablecoin holders often turn to AMMs for a simple reason. Pools can generate fee-based income from ongoing swap activity, and stable assets can make that route feel more approachable than providing liquidity to volatile token pairs.

But the operational challenge is harder than it first appears. Real AMM outcomes depend on pool depth, fee tier, and how closely onchain pricing stays aligned with external markets. Morpher's AMM explainer makes that point clearly. AMMs are liquidity-routing systems where arbitrageurs keep prices aligned, which means realized return and execution risk depend on more than headline yield in any single AMM setup.

Why manual optimization breaks down

A stablecoin holder trying to manage this by hand has to answer a lot of moving questions:

Which AMM design fits this asset pair?

Is this pool deep enough for entries and exits?

Are fees likely to compensate for execution and risk?

Has market divergence increased the chance of ugly rebalancing?

Is a different venue now offering a better risk-adjusted setup?

That isn't impossible. It is time-consuming.

For someone running treasury funds, managing cash reserves, or just trying to earn on idle USDC, the friction adds up fast. Monitoring fragmented venues, checking whether a pool still makes sense, and deciding when to rotate capital becomes a real workflow.

Where automation starts to make sense

AI-driven allocation naturally becomes a logical layer on top of AMMs. Instead of treating a pool as a static deposit destination, an automated system can treat it as one candidate inside a changing market.

One example is Yield Seeker's automated liquidity management approach, which centers on monitoring DeFi opportunities and reallocating stablecoin capital based on changing conditions. That model fits the actual nature of AMM yield. It's not "set and forget" in the pure sense. It's closer to continuous evaluation.

A useful mental model is this:

Manual stablecoin farming | Automated monitoring |

|---|---|

You check pools occasionally | A system evaluates conditions continuously |

You compare yields one venue at a time | A system can assess multiple venues together |

You react after conditions change | A system can reallocate based on predefined logic |

For readers who want a visual primer before going deeper, this short walkthrough adds context:

The bigger lesson is simple. AMM yield is an optimization problem, not just a deposit decision. Stablecoin holders earn better when they account for structure, execution, and risk together.

If you want a lower-friction way to put that into practice, Yield Seeker lets you deposit stablecoins and use an AI agent to monitor and allocate across DeFi opportunities in real time, including AMM-related strategies, without manually tracking every pool yourself.