You open a dashboard, sort by yield, and one protocol jumps out. The rate looks attractive. The interface looks polished. Then you see the headline number: a huge total value locked figure.

That number is designed to trigger confidence.

For stablecoin investors, it often does. Big TVL can feel like shorthand for safety, traction, and deep liquidity. If a lot of capital is already there, it's easy to assume the hard diligence has been done by the crowd. Sometimes that instinct helps. Sometimes it walks you straight into incentive farming, hidden concentration risk, or a protocol whose deposits are large but whose economics are weak.

TVL still matters. It's just not the final answer. If you're allocating stablecoins for yield, you need to know what TVL measures, what it misses, and when it deserves less weight than the headline suggests.

The Allure of a Billion-Dollar TVL

A large TVL number works because it compresses a messy protocol into one easy signal. Busy investors don't want to inspect every contract, trace every incentive program, and compare every vault design. TVL gives a fast answer to a hard question: is this protocol substantial, or is it empty?

That shortcut is useful. It's also dangerous.

Stablecoin investors often run into the same pattern. They compare two lending markets or vault products. One has a much larger TVL, so it feels more credible. The assumption is simple: more deposits must mean more trust, more liquidity, and lower risk. In practice, that can be true, partly true, or completely wrong depending on where the deposits came from and why they're still there.

Why the number feels so persuasive

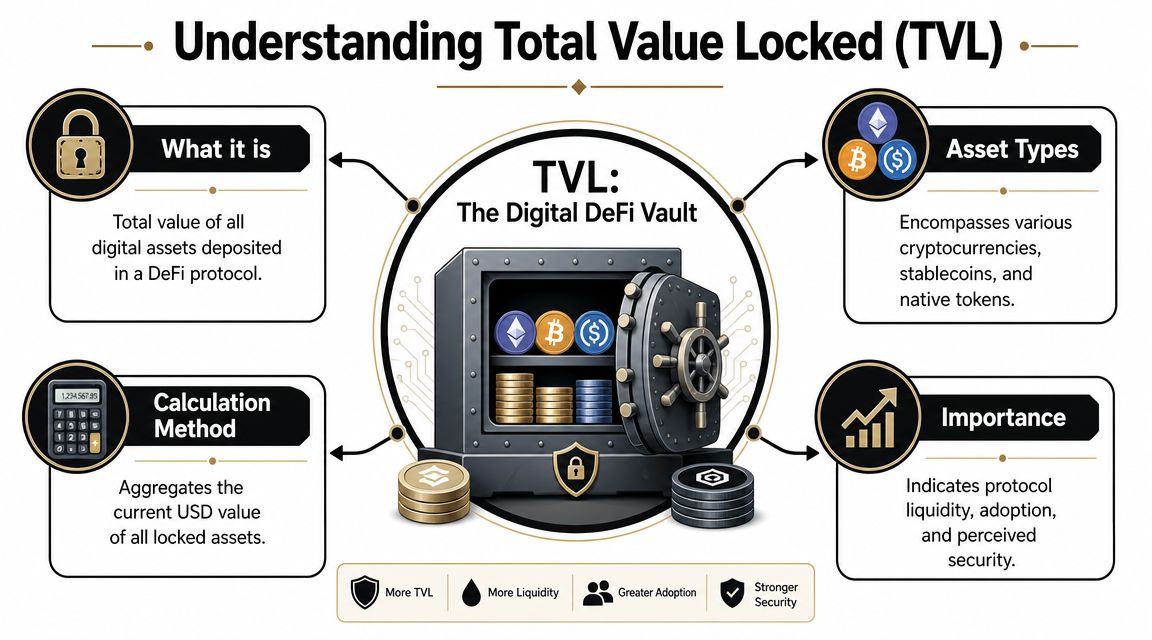

TVL became DeFi's scoreboard because it's visible and easy to compare. It tells you how much capital is parked in smart contracts across lending markets, DEX pools, staking systems, and vaults. At a glance, it looks like DeFi's version of assets under management.

That broad view also makes it useful at the market level. DeFi TVL across multiple blockchains climbed into the hundreds of billions during the boom, then fell to less than $50 billion by April 2023, which shows how tightly the metric moves with crypto prices and investor risk appetite according to Statista's DeFi TVL data.

Big TVL can signal relevance. It can also signal that a lot of money is chasing the same trade at the same time.

What a stablecoin investor should ask first

If you're deploying USDC, DAI, or similar assets, the key question isn't “is the TVL high?” It's “what kind of capital makes up that TVL?”

A protocol with large deposits may still have:

Subsidized liquidity that leaves when rewards change

Idle capital that isn't earning efficiently

Concentrated deposits controlled by a small set of wallets

Mismatch risk between stablecoin liabilities and protocol assets

For stablecoin yield, TVL is best treated as a starting filter. It tells you where capital is. It doesn't tell you whether that capital is durable, productive, or likely to remain when markets turn.

How Total Value Locked Is Calculated

TVL is a pricing exercise. Start with the assets sitting in a protocol's smart contracts, count how many units are locked, then multiply each balance by its current market price. Add those values together, and you get the protocol's total value locked, usually shown in USD so investors can compare unlike assets on one screen.

The formula is straightforward:

TVL = Σ(tokens locked × current token price)

What counts as “locked” depends on the protocol design. In a lending market, it may be supplied USDC, ETH, and wrapped BTC. In an AMM, it is the assets deposited on both sides of the pool. If you want a plain-English refresher on how those pools work, understanding liquidity pools helps. In a vault strategy, the picture gets messier because the vault may hold receipt tokens or positions that represent capital deployed somewhere else.

That last part matters more than many dashboards admit.

What the number is really measuring

TVL is not a clean measure of net new deposits. It is a mark-to-market estimate of assets currently parked in a system. If token prices rise, TVL rises even when user balances stay flat. If token prices fall, TVL drops even if nobody exits.

A simple example makes the point:

Scenario | Locked balance | Asset price | TVL contribution |

|---|---|---|---|

Before price drop | 10,000 ETH | $2,500 | $25 million |

After price drop | 10,000 ETH | $2,000 | $20 million |

The protocol still holds the same 10,000 ETH. Only the dollar value changed.

For stablecoin investors, that distinction is practical, not academic. A pool can show a lower TVL because crypto collateral repriced. A different pool can show a higher TVL because ETH rallied, not because the strategy attracted durable cash. If you are allocating USDC for yield, those are very different situations.

Where calculation gets messy

TVL looks clean on a dashboard because the final number is clean. The path to that number often is not.

Some protocols hold derivative or receipt tokens that point to assets in another protocol. Some count staked assets at the wrapper level. Some aggregate cross-chain deposits. Some data providers try to remove double counting, while others do not. A vault holding LP tokens, for example, may represent capital that was already counted in the underlying pool.

This is one reason I treat TVL as a rough sizing metric, not a precise balance-sheet figure.

Why stablecoin yield investors should care about the inputs

For a stablecoin strategy, the headline TVL matters less than the composition behind it. A billion dollars made up mostly of volatile collateral, layered borrowing, or reward-chasing deposits does not behave like a billion dollars of sticky stablecoin liquidity. Both can print the same headline number. They create very different exit conditions when markets get stressed.

That is where manual TVL reading starts to break down. To judge yield quality, you need more than the total. You need to know what assets are counted, how they were priced, whether the capital is double-counted, and how fast that liquidity can disappear. Automated, risk-aware tools like Yield Seeker are useful because they can screen those inputs continuously instead of asking investors to trust one large number on a dashboard.

Why TVL Still Matters for DeFi Investors

TVL became a default metric for a reason. Used correctly, it gives a quick read on whether a protocol has enough capital to function smoothly. For investors, that matters most in markets where liquidity quality changes the actual user experience.

What TVL can tell you at a glance

A stronger TVL often points to deeper liquidity. If you're lending, borrowing, or moving stablecoins through automated strategies, deeper liquidity usually means fewer operational headaches. Redemptions are easier. Swaps face less slippage. Borrow demand is more likely to be matched by actual available capital.

TVL also acts as a rough trust signal. Capital doesn't arrive by accident. Depositors choose where to park funds, and large pools often reflect repeated user decisions that a protocol is worth using. That isn't proof of safety, but it does tell you the market has paid attention.

For AMMs and LP strategies, this matters even more. If you want a plain-English refresher on how liquidity gets assembled and used inside DeFi markets, this guide to understanding liquidity pools is a solid companion.

Why scale can improve the product

Protocols with meaningful TVL can become easier to use because they've reached scale. More capital can support:

Better execution for swaps and rebalances

More consistent borrowing markets for lenders

Wider strategy capacity for vault products

Greater resilience when users enter or exit quickly

Those are practical benefits, not just dashboard optics.

The right way to use the signal

TVL works best as a first-pass filter. If a protocol has almost no capital, that's an immediate warning for anyone moving meaningful stablecoin size. Thin liquidity tends to magnify every other problem, from exit friction to poor pricing.

A healthy TVL can also support network effects. Users go where markets are active. Builders integrate where capital already sits. Over time, that can make larger protocols more useful than smaller rivals even before you get into detailed economics.

The key is keeping the metric in its lane. TVL can tell you that a venue is large enough to matter. It cannot tell you that the yield is sustainable, the risk is low, or the capital is there for the right reasons.

The Hidden Risks TVL Does Not Show

The biggest mistake in DeFi analysis is treating TVL like an objective truth. It isn't. It's an estimate built from assumptions, pricing inputs, inclusion rules, and sometimes data that investors can't easily verify on-chain.

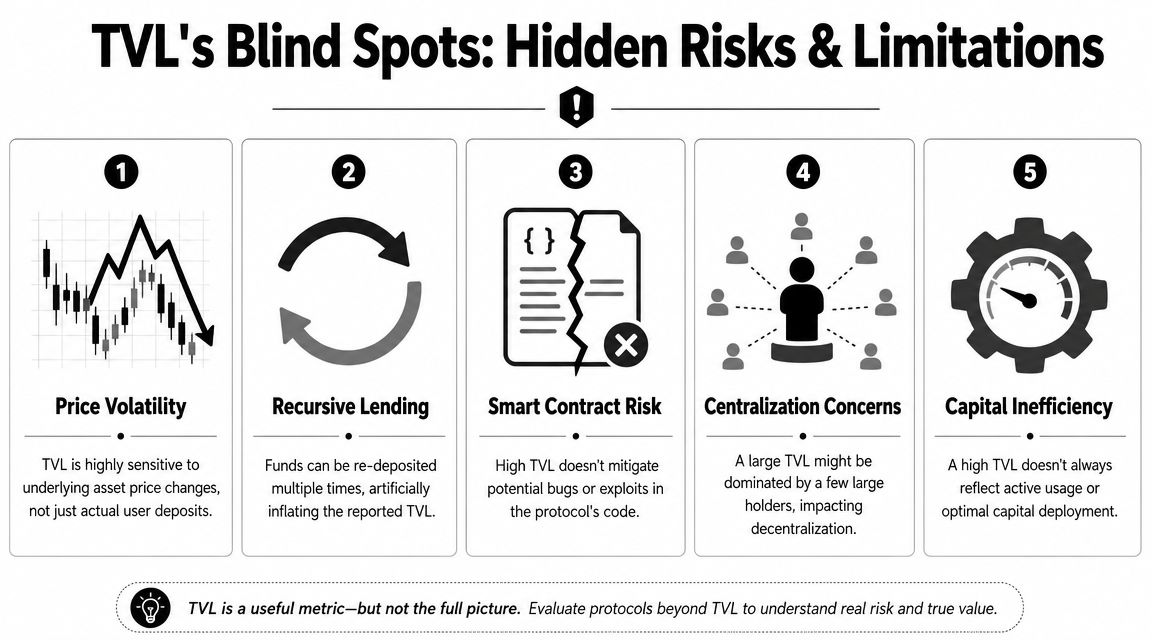

TVL can be large and still low quality

A protocol may attract deposits because rewards are high, not because users trust the product. That capital is often called mercenary capital. It arrives fast, farms emissions or bonus incentives, and leaves when the economics worsen.

For stablecoin investors, that matters because temporary deposits can make a market look deep right before it thins out. If your strategy depends on continued utilization or smooth exits, the difference between sticky deposits and rented liquidity is huge.

There's also the problem of capital inefficiency. A protocol can report a large TVL while much of that capital sits underused. In stablecoin terms, that can mean low utilization, weak revenue generation, and yields that only exist because incentives are masking weak organic demand.

A large deposit base tells you funds are present. It doesn't tell you they're productive.

Double counting and looping distort the headline

DeFi makes recursive strategies easy. Users can deposit collateral, borrow against it, redeposit the borrowed asset, and repeat. On paper, TVL rises with each layer. Economically, the system may not have gained much fresh capital.

That inflation matters when investors compare protocols by headline size alone. You may be looking at amplified capital arrangements, not genuine liquidity depth.

The same issue appears in multi-layer vault systems. One protocol deposits into another, which deposits elsewhere, and several dashboards may count parts of that stack differently. By the time the number reaches your screen, you may be seeing a padded estimate rather than a clean measure of fresh value.

A useful primer on the risk side of stablecoin strategies is this piece on understanding stablecoin risks, especially if you're evaluating yield sources that look safer than they really are.

The number itself is not standardized

This is the most important limitation. The Bank for International Settlements notes that TVL is the main metric used to assess DeFi's economic significance, but it also warns that the calculation isn't standardized and may rely on self-reported off-chain data. At the end of 2024, published estimates for Ethereum's TVL ranged from roughly $80 billion to $190 billion, a spread of over 100%, depending on the aggregator's rules and valuation approach, according to the BIS working paper on DeFi measurement.

That isn't a rounding error. That's a measurement problem.

Here's what usually drives the gap:

Inclusion rules decide which assets and protocols count

Valuation methods determine how token prices are chosen

Cross-chain treatment changes whether bridged or derivative assets are included

Self-reported data can introduce bias or manipulation risk

To see how these blind spots show up in practice, this breakdown is worth a watch:

Once you accept that TVL is a useful estimate rather than a clean fact, the investor workflow changes. You stop asking whether the number is “high.” You start asking whether it's believable, durable, and economically meaningful.

A Smarter Way to Read TVL for Stablecoin Yield

Stablecoin investors should use TVL differently from general DeFi speculators. If your goal is yield on dollar-linked assets, price swings in the asset itself matter less than protocol design, redemption quality, utilization, and whether the yield has a real source.

That's why TVL should be demoted from headline answer to context signal.

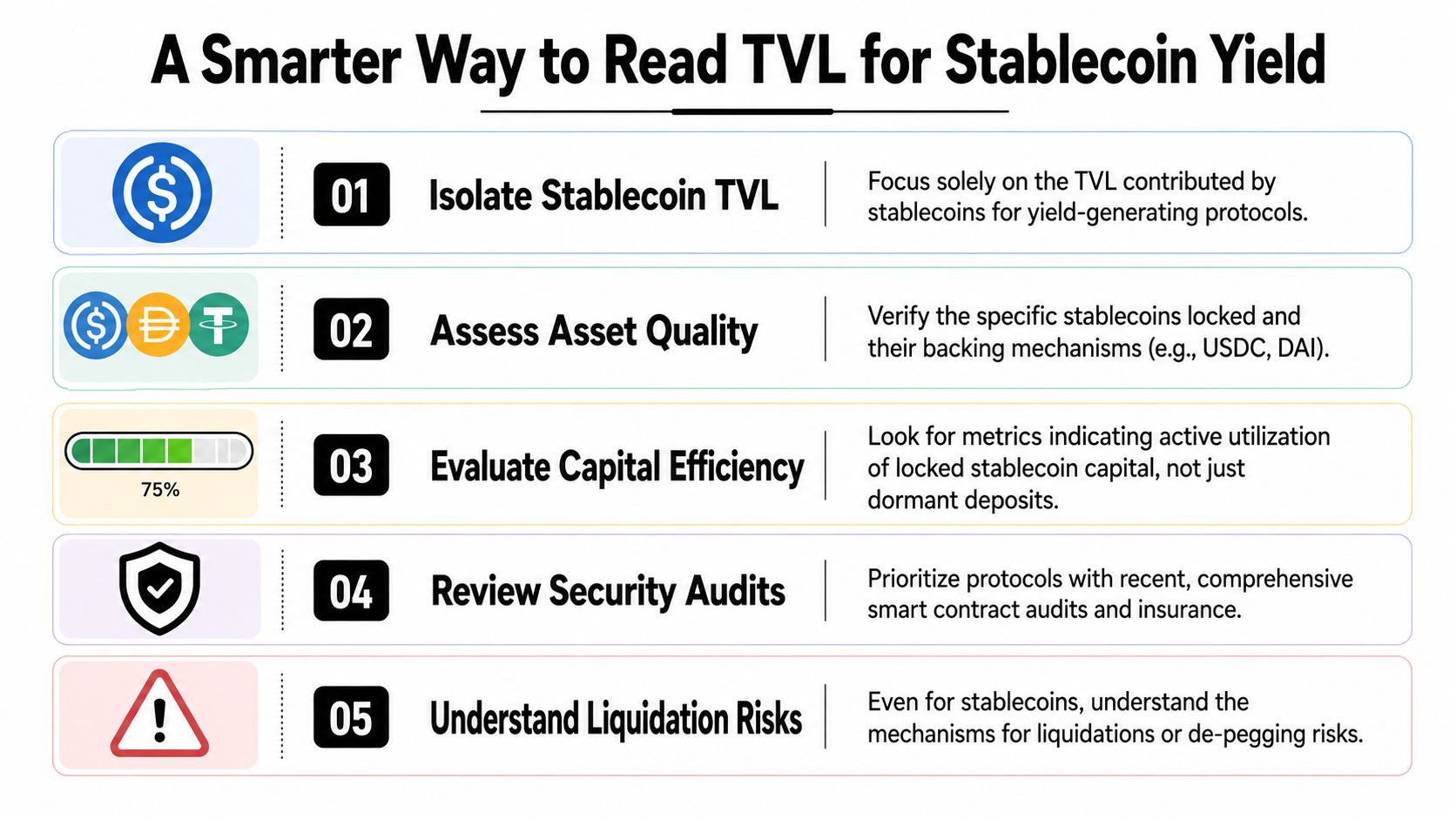

Read TVL through a stablecoin lens

A large protocol-wide TVL can hide the fact that only a small share is stablecoin capital. If you're allocating USDC, you care less about the gross total and more about the part of the system tied to your strategy.

Start by separating three questions:

Question | Why it matters for stablecoin yield |

|---|---|

Is the relevant TVL actually stablecoin-based? | Mixed-asset TVL can make a venue look safer than your segment really is |

Is the capital being used efficiently? | Idle deposits often mean weak organic yield |

Is the yield supported by activity or by incentives? | Incentive-led rates tend to be less durable |

Academic critique is moving in this direction too. Some research now questions how relevant TVL is for predicting returns, especially in stablecoin strategies where protocol risk and capital efficiency matter more than simple capital depth, as discussed in this overview of the growing critique of TVL.

What to pair with TVL

If you're screening a stablecoin opportunity, TVL becomes more useful when paired with operational metrics. The exact dataset varies by protocol, but the framework is consistent.

Look for signals like these:

Revenue quality. Is the protocol earning from real borrowing, trading, or vault activity, or mostly distributing token incentives?

Utilization. Are deposited stablecoins actively used, or mostly parked?

Withdrawal realism. Can users leave smoothly during stress, or does liquidity dry up when it's needed?

Collateral quality. If the system depends on volatile assets elsewhere, stablecoin depositors still inherit that risk.

Distribution of deposits. Broad capital is usually healthier than a pool dominated by a few large wallets.

A deeper framework for this kind of screening appears in this guide on TVL tracking signals, especially if you want to move from raw dashboard watching to actual decision rules.

Working heuristic: For stablecoin yield, TVL tells you where money is parked. Revenue, utilization, and redemption behavior tell you whether that parking lot is a business.

When to ignore a big TVL number

Sometimes the best use of TVL is knowing when not to care about it.

If a protocol shows high TVL but the yield depends on temporary token emissions, if the stablecoin share is unclear, or if capital efficiency looks weak, the headline figure shouldn't carry much weight. In those setups, TVL is more of a marketing layer than an investment signal.

Stablecoin investors do better when they ask narrower questions. What backs the yield? What can break the redemption path? What happens if incentives drop? Those questions usually reveal more than a giant TVL badge on a homepage.

Automating Beyond TVL with Yield Seeker

A stablecoin investor can read TVL correctly and still lose time, miss risk shifts, or stay too long in a weakening pool. The problem is not the definition. The problem is keeping up with changing rates, liquidity, incentives, chain conditions, and venue-specific risk across a portfolio that moves every day.

Manual analysis breaks down once capital is spread across several protocols or chains.

Why hand-checking breaks down

The Bank for International Settlements warns that TVL calculations are not standardized and can rely on self-reported data, which means investors need to pair TVL with metrics such as active users, trading volume, and revenue to judge real economic activity, as noted in the BIS discussion of DeFi data quality.

For a stablecoin allocator, that turns a simple screen into an ongoing operating job. A pool can keep its TVL while its yield mix gets worse. A vault can look stable until exit liquidity thins out. Incentives can mask weak organic demand for longer than many depositors expect.

None of that is hard to understand in isolation.

It becomes hard when you have to monitor all of it at once, update your view quickly, and act before the market reprices the opportunity.

What automation should actually do

Useful automation treats TVL as a context signal, not a decision rule. It should monitor the quality of yield, the durability of liquidity, and the conditions that matter to a stablecoin holder who may need to rotate out fast.

That usually means:

Tracking TVL alongside revenue, utilization, and incentive dependence

Flagging changes in risk, not just changes in headline APY

Adjusting allocations as conditions improve or deteriorate

Reducing dashboard sprawl so decisions happen on time

Keeping funds accessible instead of burying them in rigid strategies

Yield Seeker follows that approach. It uses an AI-driven agent to monitor and allocate stablecoin capital across DeFi venues in real time, with TVL treated as one input inside a broader risk process. For broader context on how to use AI for investing, that guide explains where automation helps and where human judgment still matters.

For stablecoin yield investors, the practical use of TVL is simple. Use it to spot where capital is gathering. Ignore it as a standalone proxy for safety or yield quality. Tools like Yield Seeker matter because they keep checking the parts TVL misses, then act on those changes faster than a manual spreadsheet can.

If you want a simpler way to put that into practice, Yield Seeker helps automate stablecoin yield decisions beyond raw TVL. You can deposit USDC on Base, keep funds accessible, and let an AI agent monitor DeFi opportunities with a risk-aware approach so you do not have to compare every protocol, dashboard, and rate change by hand.